Implied vs Historical Volatility

Use volatility to your advantage!

Volatility, as many traders can attest to, can make you feel like a hero or a zero; it all depends on which side you are positioned.

First, let’s define them both.

Historical Volatility (HV) - A statistical measure of the dispersion of returns for a stock over a given period of time.

Implied Volatility (IV) - Shows how the market views where volatility should be in the future and helps gauge the sentiment about the volatility of a stock or the market. This is an estimate and is commonly used in pricing options. Often referred to as “vol” - NOT to be mistaken for volume.

If you are interested in how they are calculated in order to gain a better understanding, there are plenty of resources online - we won’t be getting into that during this article.

What are they used for?

Think of HV as the rate of change of the underlying stock. Every stock has its own pulse, hence, the higher the level of HV, the more that stock has moved (either up or down) in recent history. From this understanding, we can gather that, theoretically, that stock will move in a similar fashion into the future - from a magnitude perspective and not in any way indicating the direction of that movement.

The stark difference between the two (if you choose to take only one piece of knowledge from this post, THIS should be it), is that Historical Volatility is a historical measure of volatility - it is a fact and cannot be changed since this price movement has already happened and can be found on a chart. Implied Volatility, on the other hand, is forward-looking and therefore helps gauge the sentiment about the volatility of a stock.

Most trading platforms will have both the HV and IV available as part of their charting package and can be displayed as a visual below the price chart.

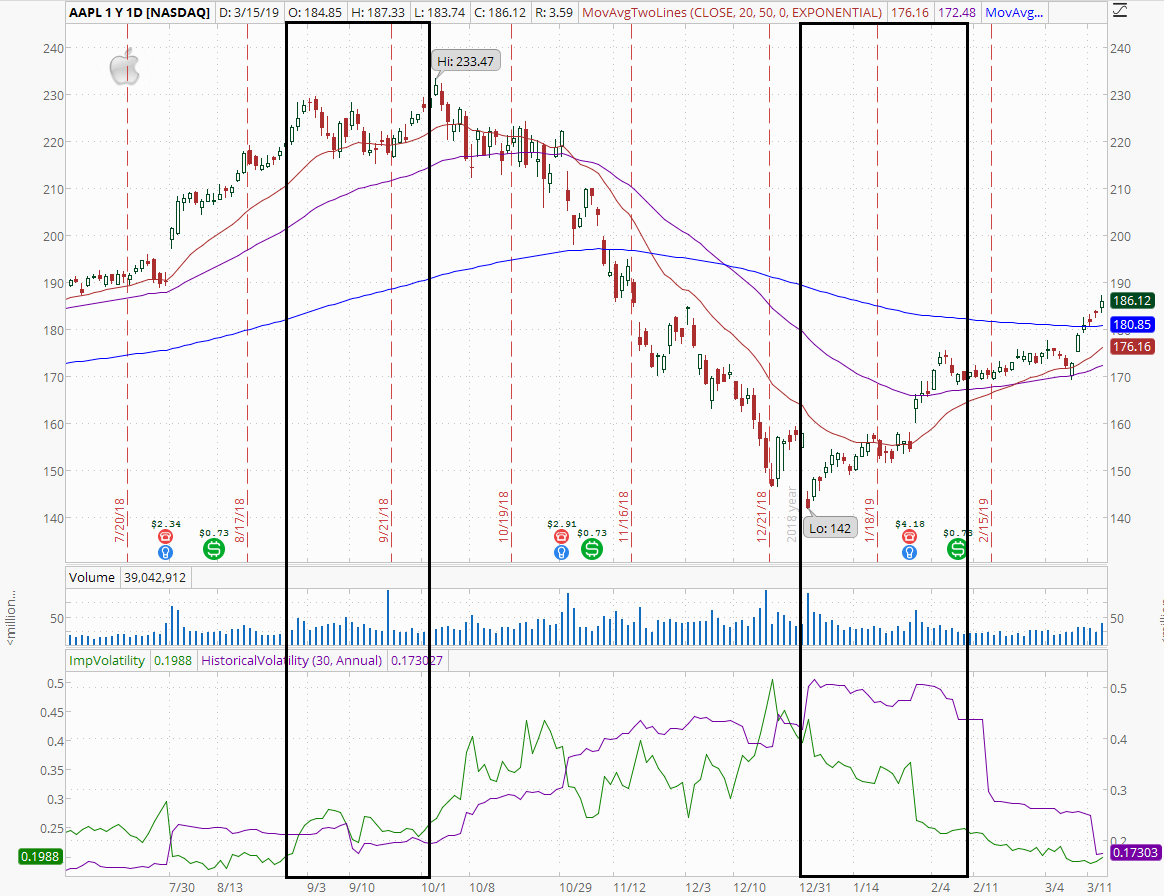

Let’s take a look at the AAPL chart below as an example.

The purple line at the bottom of the image is the Historical Volatility and the green line is the Implied Volatility. Notice the two lines tend to cross over each other several times over the period. This essentially means that (implied) volatility is expected to be greater than it has recently been (historical volatility); the green line is above purple. Vice versa is true if the expected volatility is anticipated to be lower than the historical. More about the relationship between the two can be found in our post about the Implied Volatility ratio.

The highlighted area on the left shows a period with relatively low historical volatility. Notice the price range during the preceding days was relatively narrow, hence the low HV. Now pay attention to the highlighted area on the right side and the stark difference in the price range preceding that - the range is significantly higher, hence the high HV.

As described above, due to its nature IV can fluctuate significantly quicker than HV. Implied Volatility is not directly observable so in order to solve for it, we need to use an option pricing model. InteractiveBrokers has a great options calculator you can play around with to study the effects on option prices by modifying any of the inputs. You can access it by clicking HERE.

The bottom line is in order to trade options profitably, you have to have a thorough understanding of both implied and historical volatility (current and historical) and how it contributes to option pricing.

Stay tuned for more in-depth posts about volatility and how to use it to your benefit.

If this was useful to you, please LIKE and share below.